ABSTRACT

The paper discusses how conventional lending frameworks can be applied to the modern microfinance models to enhance the financial inclusion of the underserved communities. There was the mixed methods approach, which included 200 rural and semi-urban borrowers. Findings revealed that rotating savings and credit associations (ROSCAs) represent the most widespread traditional lending system, and hybrid microfinance models have a major positive effect on the rate of repayment, financial literacy, and customer satisfaction. Nevertheless, such issues as regulatory bottlenecks, urban scalability and dependence on social networks must be overcome to implement it sustainably.

Keywords: Microfinance, Traditional Lending, ROSCAs, Financial Inclusion, Borrower, Satisfaction, Hybrid Models.

Introduction

Microfinance has emerged as an important tool in facilitating financial inclusion, especially to the low-income earners who do not have the access to the mainstream banking services. Informal and traditional lending practices are still a major aspect of community finance although formal microfinance institutions (MFIs) are proliferating. These local-based practices based on local customs and networks of trust have long been systems of access to credit, savings accumulation and social cohesion.

This research is aimed at discussing the way in which the models of microfinance can be improved with references to the use of the traditional lending practices. The research attempts to suggest sustainable models, integrating both the efficacy of the modern microfinance and the social capital of the traditional lending, by discussing the merits and shortcomings of these conventional systems.

Literature Review

Kandie and Islam (2022) discussed how microfinance has evolved into digital microcredit and how it is influencing the reduction of poverty. It discloses that digital platforms increase credit access, lower transaction costs, and financial access, thus making the economic vulnerability of underserved communities less complex and subjecting the conventional lending practices to a transformation.

Lawhaishy and Othman (2023) presented an Islamic microfinance-based microfinance model among the Libyan MSMEs, which is consistent with the Shariah principles and contributes to entrepreneurship. The model eased access to capital, promoted ethical investment behaviour, and reinforced trust between lenders and borrowers, indicating the promise of faith-based financial models in the situations when traditional microfinance might receive social/cultural opposition.

Mia (2024) investigated the process of Islamic microfinance transformation to conventional microfinance in Bangladesh and offered models of Shariah compliance. It also emphasizes the advantages of working religious doctrines in microfinance especially in religious communities. This paper concludes that the Islamic microfinance does not only sustain the social goals, it also increases financial sustainability, repayment, and communal trust.

ResearchMethodology

The researchers used a mixed-methods design to study the conventional lending integration into microfinance by examining 200 borrowers by gathering questionnaire, focus group, and interview data.

3.1 Research Design

The research design employed in the study to examine how traditional methods of lending have been integrated in the modern-day microfinance models with respect to the participation of the borrowers, their satisfaction, financial literacy, and difficulties in the adoption of the hybrid microfinance models.

3.2 Population and Sample

This paper sought to identify micro finance borrowers and traditional lending system members of rural and semi urban areas, and purposive sampling method was used to identify 200 respondents who had experience in traditional lending, modern micro finance or both.

3.3 Data Collection Methods

The research employed structured questionnaires to obtain quantitative data on participation, repayment, financial literacy, satisfaction, challenges, borrower experiences, social dynamics, trust mechanism, key informant interviews with microfinance officers, and community leaders in order to verify findings and find practical solutions.

3.4 Data Analysis

The analysis study focused on descriptive statistics to analyze quantitative data and thematic analysis to analyze qualitative data to establish patterns in borrower experiences, trust mechanisms and institutional barriers and demonstrate participation, impact and challenges.

DataAnalysis and Interpretation

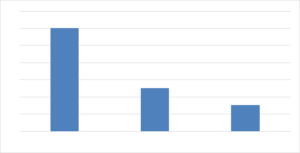

Figure 1 and Table 1 show how the respondents were involved in different traditional lending activities. The figures indicate that most of them (60 percent) were engaged in ROSCAs, after which came cooperative lending groups (25 percent) and family-based lending (15 percent).

Table 1: Participation in Traditional Lending Practices

| Traditional Lending Practice | Number of Respondents | Percentage (%) |

| ROSCAs | 120 | 60 |

| Cooperative Lending Groups | 50 | 25 |

| Family-Based Lending | 30 | 15 |

| Total | 200 | 100 |

Figure 1: Graphical Representation of Participation in Traditional Lending Practice

ROSCA is the most popular and reliable type of traditional lending since it is simple, repeated, and require social trust, whereas cooperative groups and family-based lending cater to smaller sections of the community as there is a difference in availability and reliance on social networks.

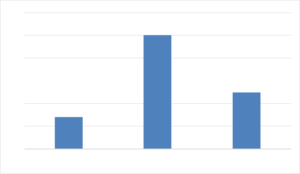

Table 2 and Figure 2 give the results of integrating traditional lending businesses on the modern microfinance models. The three most important indicators, including the rate of repayment, financial literacy, and satisfaction of the borrowers, improve significantly following the integration.

Table 2: Impact of Hybrid Microfinance Models on Borrowers

| Indicator | Before Integration | After Integration | % Improvement |

| Repayment Rate (%) | 78 | 92 | 14% |

| Financial Literacy Score (1-10) | 5.2 | 7.8 | 50% |

| Borrower Satisfaction (%) | 68 | 85 | 25% |

Figure 2: Graphical Representation of Impact of Hybrid Microfinance Models on Borrowers

It is revealed that hybrid microfinance models have a more significant positive impact on the outcome of the borrowers such as higher repayment, better financial literacy through group interactions, guided, and better overall satisfaction through higher trust and support in the lending system.

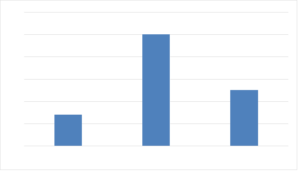

According to Table 3 and Figure 3, key limitations to the incorporation of the traditional lending model into the modern microfinance model are regulatory restrictions (35%), low scale (30%), in urban centers, social network dependence (20%), and aversion to formal banking processes (15%).

Table 3: Challenges in Integrating Traditional Lending into Microfinance

| Challenge | Frequency | Percentage (%) |

| Regulatory Restrictions | 70 | 35 |

| Limited Scalability in Urban Areas | 60 | 30 |

| Dependence on Strong Social Networks | 40 | 20 |

| Resistance to Formal Banking Procedures | 30 | 15 |

| Total | 200 | 100 |

Figure 3: Graphical Representation of Challenges in Integrating Traditional Lending into Microfinance

The traditional lending has its advantages but it could be challenged logistically and socially within the formal microfinance systems. The broader application of hybrid microfinance models and their sustainability is important metrics that need to be addressed through regulatory constraints and proper model adaptation to urban settings.

Conclusion

The paper recommends that incorporation of traditional lending systems such as ROSCAs, cooperative groups, and family lending into the modern microfinance systems can enhance financial access, loan repayments, and customer satisfaction. The hybrid models draw on trust, social cohesion and accountability of traditional systems but enjoy the benefits of formal microfinance structure. Nonetheless, such issues as regulatory limitations and reliance on social networks should be taken to make the implementation sustainable.

Statements & Declarations:

Peer Review Statement: This article has undergone a double-blind peer review process. The identities of both authors and reviewers were concealed throughout the review process to ensure impartiality, academic integrity, and objectivity.

Competing Interests / Conflict of Interest: The author(s) declare that there are no known competing financial or non-financial interests that could have influenced the work reported in this paper.

Funding Statement: This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.

Data Availability Statement: The data supporting the findings of this study are available from the corresponding author upon reasonable request.

License Statement: This article is published under the terms of the Creative Commons Attribution–NonCommercial–NoDerivatives 4.0 International License (CC BY-NC-ND 4.0), which permits non-commercial use, distribution, and reproduction in any medium, provided the original work is properly cited and no modifications or adaptations are made.

References:

- Strategic approaches to enhancingcredit risk management in microfinance institutions. International Journal of Frontline Research in Multidisciplinary Studies, 4(1), 53–62. https://doi.org/10.56355/ijfrms.2024.4.1.0033

- Kandie, D., & Islam, K. J.(2022). A new era of microfinance: The digital microcredit and its impact on poverty. Journal of International Development, 34(3), 469–492. https://doi.org/10.1002/jid.3607

- Lawhaishy, Z. B., & Othman, A. H. A.(2023). Introducing an Islamic equity-based microfinance models for MSMEs in the State of Libya. Qualitative Research in Financial Markets, 15(1), 1–28. https://doi.org/10.1108/QRFM-01-2021-0017

- Mia, A. (2024). The transformation of conventional microfinance into Islamic microfinance in Bangladesh: Proposed Shariah-based model (s). Qualitative Research in Financial Markets, 16(3), 565–585. https://doi.org/10.1108/QRFM-06-2022-0104

- Singh, J., Dutt, P., & Adbi, A.(2022). Microfinance and entrepreneurship at the base of the pyramid. Strategic Entrepreneurship Journal, 16(1), 3–31. https://doi.org/10.1002/sej.1394

- Sinha, (2020). Study of the Functionally Effective Credit Lending Models of microfinance. International Journal of Business Insights & Transformation, 13(2).

- Uddin, M. J., Vizzari, G., Bandini, S., & Imam, M. O.(2018). A case-based reasoning approach to rate microcredit borrower risk in online Kiva P2P lending model. Data Technologies and Applications, 52(1), 58–83. https://doi.org/10.1108/DTA-02-2017-0009

- Uddin, M. N., Hamdan, H., Embi, N. A. C., Kassim, S., & Saad, N.(2020). Governance structure of microfinance institutions: A comparison of models and ıts implication on social impact and poverty reduction. İbn Haldun Çalışmaları Dergisi. Journal of Ibn Haldun Studies, Ibn Haldun University, 5(1), 95–118. https://doi.org/10.36657/ihcd.2020.68

- Uddin, M. N., Hamdan, H., Saad, N. B., Haque, A., Kassim, S., Embi, N. A. C., & Agarwal, K.(2022). The governance structure of microfinance institutions: A comparison of models of sustainability and their implication on outreach. Asian Journal of Economics, Business and Accounting, 22(19), 104–123. https://doi.org/10.9734/ajeba/2022/v22i1930662

- Wanke, P., Hassan, M. K., Azad, M. A. K., Rahman, M. A., & Akther, N.(2022). Application of a distributed verification in Islamic microfinance institutions: A sustainable model. Financial Innovation, 8(1), 80. https://doi.org/10.1186/s40854-022-00384-z

- Mehta, S. (2025b). The future of fair value accounting in a digital economy. Shodh Sari-An International Multidisciplinary Journal, 04(02), 334–365. https://doi.org/10.59231/sari7828